Are you a brand in fashion, lifestyle or retail taking sustainable steps to make an impact? Do you find it challenging to comply with this new set of regulations? Do you want to know how reporting on business-critical topics affects key stakeholders? Are you looking for practical advice and tools?

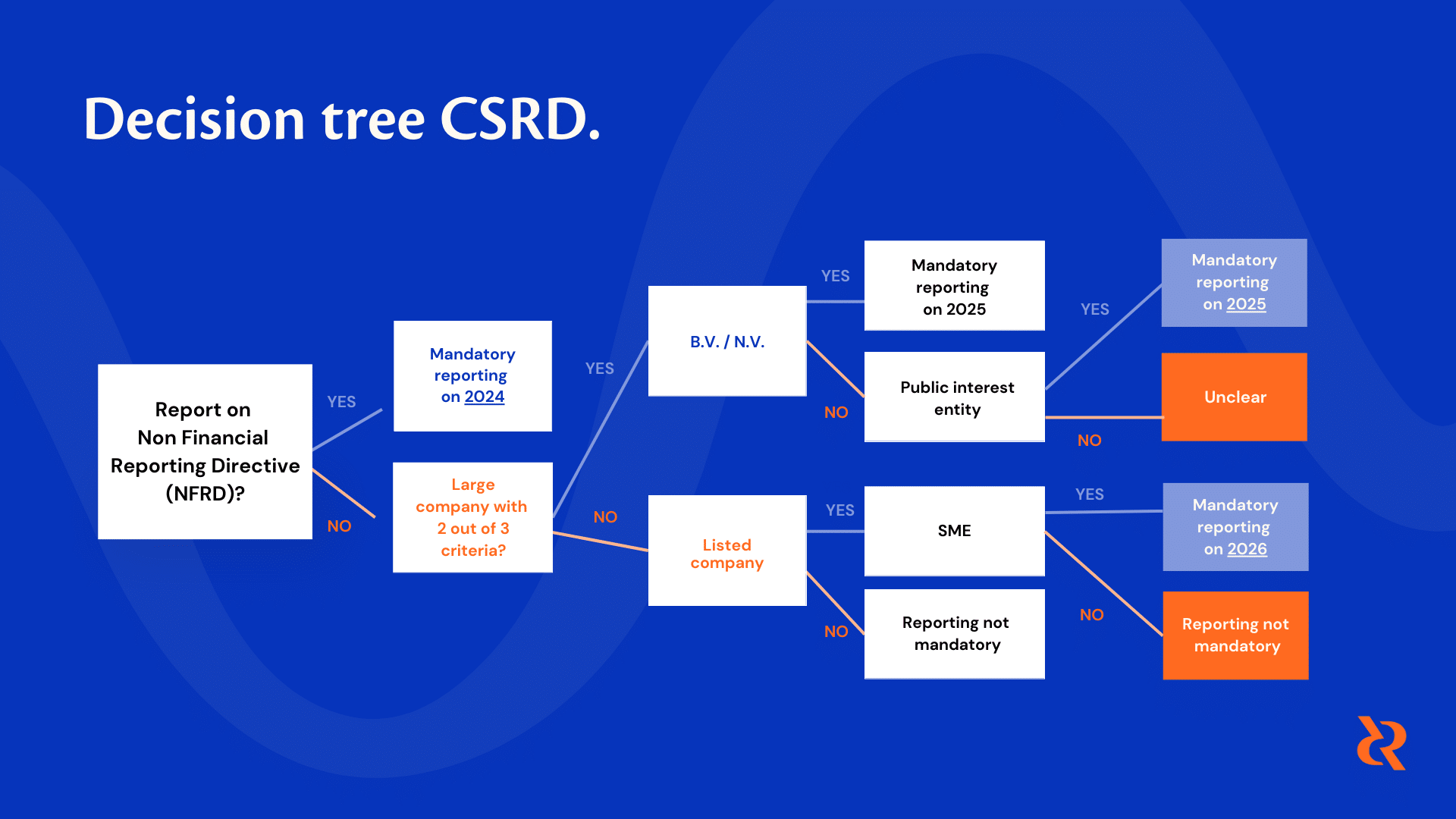

The law, The Corporate Sustainability Reporting Directive (CSRD) requires all large companies to publish regular reports on their environmental and social impact activities, and it helps investors, consumers, policymakers, and other stakeholders evaluate large companies’ non-financial performance.

With the exception of micro-entities, the CSRD proposals significantly expand the scope of the existing Non-Financial Reporting Directive (NFSD) rules to cover all large undertakings as well as all those listed on EU regulated markets.

You might wonder how to navigate all this.

We are here to help you!

Here is a brief overview of the key changes and impacts from the CSRD:

Which companies will be applicable?

- all EU limited liability companies with 500 or more employees and €150 million or more in worldwide net turnover.

- limited liability companies operating in defined high-impact sectors, including mining and extractives, agriculture and textiles, that have more than 250 employees and a net turnover of €40 million or more worldwide.

- listed companies (Small and medium listed companies get an extra 3 years to comply)

How many companies are subject to the new directive (EU)?

Close to 50 000 companies

Covering >75% of total EU companies’ turnover

What is the scope of the reporting requirements?

Companies should report on (adding additional information from current EU Directive):

- Double materiality concept

- Process to select material topics for stakeholders

- More forward thinking information e.g. targets

- Disclose information relating to intangibles

- Reporting in line with Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy Regulation

Is independent 3rd party assurance mandatory?

Mandatory – limited level of assurance

Including:

- Integration in Auditor’s Report

- Involvement of key audit partner

- Scope to include EU Taxonomy and process to identify key relevant information

Where should companies report?

Inclusion in the Management Report

What format should companies report?

To be submitted in electronic format

(in XHTML format in accordance with ESEF Regulation)

Start taking action now

It’s better to start earlier than later. Contact us for a tailored solution regarding upcoming regulations.